For most of us, over the past year the Covid-19 pandemic has understandably overshadowed all other concerns.

But new research from the Swiss Re Institute makes it clear climate change will be the fundamental economic challenge of our time – and measures just how high a price our region will face if we fail to address it. How all of us, re/insurers included, respond to this test will define Asia’s growth trajectory, and foster, or endanger, the prosperity of future generations.

If this sounds urgent, it’s because the stakes couldn’t be higher. Our report, The economics of climate change: No action not an option, takes research on climate risk factors – including physical risks such as damage to property – and sets those against economic data to create a unique assessment of how climate resilient the world’s major economies are.

The main outcome, our Climate Economics Index, ranks 48 economies according to how severely their GDP is likely to be impacted by climate risk factors by 2050, if no steps are taken to mitigate these risks. Particularly for our region, the results make for sobering reading.

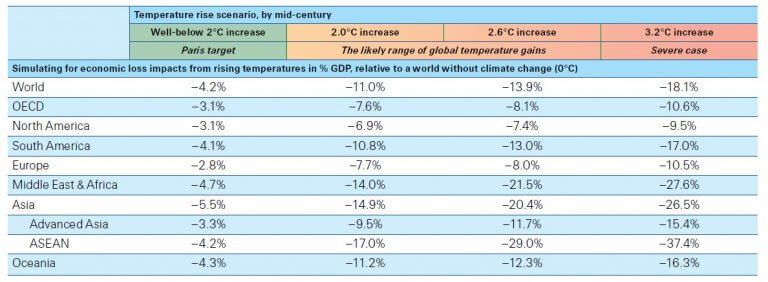

Under the most negative ‘business as usual’ scenario, climate change will cost Asia more than a quarter (26.5%) of GDP by 2050. That’s the highest regional toll after the Middle East and Africa (27.6%).

Note: Temperature increases are from pre-industrial times to mid-century, and relate to increasing emissions and/or increasing climate sensitivity (reaction of temperatures to emissions) from left to right. Source: Swiss Re Institute

Emerging Asia will bear the brunt of climate change impacts. Due to a combination of geography and lack of adaptive capacity such as climate mitigation infrastructure, markets like Indonesia, Malaysia, Thailand and the Philippines rank on the low end of the Index.

However, the research demonstrates conclusively that there are no winners in a world of rising temperatures. In a most severe scenario, Japan would lose 12% of GDP by mid-century, Australia 16.5%, and Singapore 46.4% – roughly the same proportion as its less prosperous Southeast Asian neighbours.

The case for transformation

Faced with numbers like these, it’s easy to conclude there’s little we can do to turn an overwhelming tide. But I’d prefer to see the research as a call to action, and believe it also contains positive messages that can serve us well.

The first is that we really are all in this together. With climate change set to inflict heavy costs on the global economy, it’s in every nation’s interest to invest in the policies and infrastructure to rein in temperature gains. Quantifying the costs of climate change will build the economic case for these kinds of investments.

Another important takeaway is that Asia can lead the way in climate change mitigation. China and India are two of the world’s largest economies and largest emitters. Together they can play a decisive role in the global effort to meet the Paris Agreement targets – an achievement that could avert losses up to 14% of GDP worldwide.

The research also shows that how companies manage the transition to a lower-carbon economy will be critical. Like economies, businesses are presented with a choice; to carry on with ‘business as usual’ and face earnings pressure due to carbon taxes and stranded assets; or to boost investment in sustainable energy sources and technologies, positioning themselves to benefit over the longer-term.

How insurers can change the risk equation

Re/insurers have much to contribute to enhancing our societies’ climate change resilience. By closing the region’s protection gap, which stands at some USD 60 billion in Asia,[1] our industry can support businesses and households to bounce back and focus on rebuilding should natural disasters strike.

Major natural catastrophes tend to dominate the headlines, but according to Swiss Re Institute, it was small to mid-size events, or secondary perils, that were responsible for almost three-quarters of disaster-related losses in 2020. Many secondary perils are connected to the rise of both drier and wetter weather, and may exacerbate the impact of primary perils.

As risk managers, underwriters and investors, re/insurers need to be at the forefront of efforts to assess the likelihood and impacts of disaster events of all sizes. By developing sophisticated models and data-based tools to gauge climate-related risks at a more granular level, we can assist governments and businesses to mitigate and adapt – whether by formulating underwriting solutions for emerging hazards; analysing damages and claims patterns to anticipate trends; or sending risk signals that encourage behavioural changes.

Our CatNet® tool, an online atlas that combines satellite imagery with hazard, loss and exposure data to give clients a snapshot of the risks in various regions, is an example of the power and transparency technology can offer. We are constantly advancing this platform, most recently striking a partnership with ICEYE, a global leader in applying satellite-based technology to monitor flooding, that will leverage its data to enhance risk mitigation, disaster response and claims processing.

Innovations like these will help us protect and invest in the promising infrastructure and industries emerging in the upcoming climate transition. That said, even the best data and tools will do little to help us assess and quantify the nature of the risks if customers are reluctant to adopt and pay for them. The increased frequency and severity of primary and secondary events proves we must view these solutions as a shared and necessary investment, and that insurance can only be part of a much bigger, more holistic push to mitigate climate change impacts.

All of us – re/insurers, governments, regulators, businesses, communities and individuals – need to act as an ecosystem to not just advance risk knowledge, but also to prepare for the risks. We all have a role to play in building societal resilience and laying the foundation for faster and more effective disaster recovery.

My hope is that our research contributes to a better understanding of the risks climate change poses to the region, and a stronger resolve to face these issues head on, as an industry and as a global community. As our report demonstrates, transition will not be without its pain points – but the cost of inaction would be even higher.

This article was written by Russell Higginbotham, CEO reinsurance Asia and regional president Asia, Swiss Re who is based in Singapore.

[1] sigma 1/2021 Natural catastrophes in 2020: secondary perils in the spotlight, but don’t forget primary-peril risks; Swiss Re Institute

-

Risk management: Insurance lessons from one of China’s deadliest industrial accidents in recent years

- July 20

The explosion at a Chinese fireworks factory at the start of May is a reminder that the true value of an insurance program is tested not when a policy is purchased, but when catastrophe strikes. The fire at the Huasheng Fireworks Manufacturing and Display Company in Liuyang, Hunan province, claimed 37 lives, injured 51 people, […]

-

Insurtech: 6 AI trends reshaping the industry

- February 25

AI has become the defining technology of our time, entering the hands of everyday consumers and employees faster than any innovation in recent history. The speed of adoption has been remarkable, mirrored by an equally intense wave of hype, but real business impacts are beginning to surface. What was once the domain of specialised data […]

-

AI: Complexity mismatch amid the case for augmenting the investment office

- January 21

With prudent oversight and strong guardrails, an augmented investment office can allow insurers to confidently ride the private credit boom without being undermined by the complexity they have embraced.

-

Marine: Amid backlogs and breakdowns, Covid-19 maintenance delays put vessel safety at risk

- December 9

Asia is at the sharp end of a hidden maritime risk, with post-pandemic machinery-related losses becoming an even more significant issue.

-

Beazley | Clean marine: How aqua-innovators can ride the energy wave

Insurance is critical to clean marine progress, but new fuels bring risks traditional policies do not fully cover, presenting market players an opportunity to build new models.

-

PartnerRe | Dementia the protection gap insurers can no longer ignore

Unlike acute illnesses, dementia creates a long tail of financial need and its impact extends well beyond patients.

-

Sedgwick | Investing in people is shaping the future of loss adjusting in Asia

Sedgwick Asia says it is ready to meet the evolving challenges of Asia’s dynamic insurance markets.

-

PartnerRe | Understanding ageing in APAC: why perception, planning and protection don’t always align

Ageing is shaping finances, family dynamics and insurance needs of the caregiving ecosystem, but current product propositions and underwriting frameworks are not keeping pace with protection needs, finds PartnerRe survey.

Russell Higginbotham, Swiss Re

Climate change: the real costs to Asia Pacific

Russell Higginbotham, Swiss Re